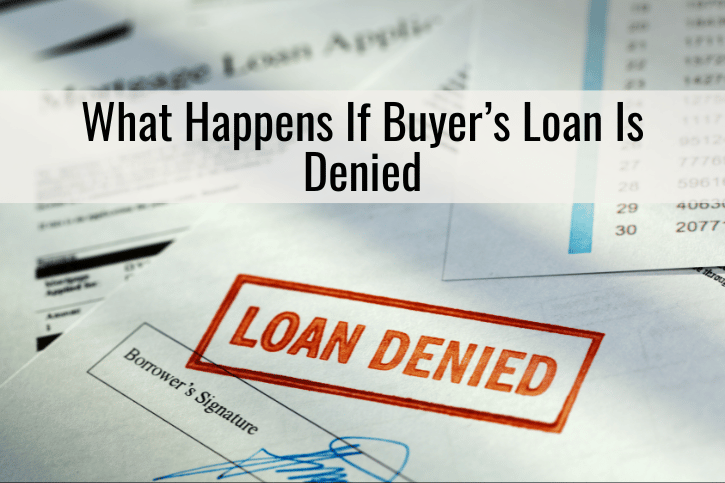

As a seller, there are few moments more deflating than hearing your transaction is off—especially when you’ve cleared the inspection, negotiated every detail, and already packed half your house. Yet it happens more than many expect. What happens if buyer’s loan is denied? It’s a question every seller should ask before accepting an offer. The reality is that buyer financing falling through isn’t just inconvenient. It can disrupt your timeline, weaken your negotiating position, and send you back to square one.

Financing is the lifeblood of most real estate transactions. Without it, there is no sale. When a lender says “no,” everything unravels. But it doesn’t have to catch you off guard. In fact, if you take a proactive and strategic approach, you can reduce your exposure to risk—sometimes significantly.

And that’s where expertise matters.

TLDR: What Happens If Buyer’s Loan Is Denied

-

A buyer’s loan denial can derail your home sale and force you to relist, costing time and momentum.

-

Understanding buyer financing falling through is essential to protect your transaction as a seller.

-

Proactive preparation and smart contract structuring are key to minimizing risk.

-

There are red flags sellers can watch for to catch financing issues early.

-

Robbie English, Broker and REALTOR at Uncommon Realty, provides expert guidance to ensure sellers avoid the fallout from failed financing.

The Seller’s Side of a Loan Denial

Let’s put ourselves in the seller’s shoes for a moment.

You list your home, field showings, endure negotiations, and finally get under contract. You’re relieved. You make plans. Maybe you’re purchasing another home yourself. Maybe you’re coordinating movers, painters, or contractors. Then the call comes in—your buyer didn’t get final loan approval.

You’re now facing the loss of weeks of market time and the emotional toll of uncertainty. Worse, you might have to relist in a market that now views your property with suspicion: “Why is it back on the market? Was something wrong with it?”

The reality? It may have nothing to do with your home. And everything to do with a buyer who couldn’t close.

Why Buyer Financing Falls Apart

Buyer financing falling through usually happens for one of three reasons: poor pre-approval, changes in the buyer’s financial condition, or lender-specific issues. Most buyers begin the process with a pre-qualification or pre-approval letter, but not all pre-approvals are created equal. Some are little more than a buyer stating their income and debts verbally. Others are fully underwritten and verified by a mortgage professional.

As a seller, you don’t control the buyer’s lender, job stability, or creditworthiness. But you can ask the right questions, request the right documentation, and work with an experienced broker who knows how to recognize when financing might be on shaky ground.

How to Reduce the Risk of a Failed Buyer Loan

It’s not about being pessimistic—it’s about being prepared.

The risk of buyer financing falling through doesn’t have to be paralyzing. In fact, it can often be managed with thoughtful planning. Here’s how:

-

Always require a strong pre-approval letter that is fully underwritten, not just a basic pre-qualification.

-

Ask whether the buyer’s lender has already pulled credit, verified employment, and analyzed bank statements.

-

Choose lenders with reputations for communication and speed—some big-name lenders are known for delays and red tape.

-

Consider backup offers. If your market allows it, having a second approved buyer waiting in the wings gives you leverage.

-

Pay attention to the buyer’s contingencies. Financing contingencies often give buyers a broad window to back out—narrowing that window can protect your position.

What Happens If Buyer’s Loan Is Denied Midway Through?

It depends on how your contract is structured.

In many standard agreements, the buyer has an option or financing period during which they can back out if their loan is denied. If the denial occurs within that period, they typically receive their earnest money back. If it happens outside of that window, they could lose their deposit—and you might be entitled to damages.

But collecting that money doesn’t erase the weeks lost or the new uncertainty you face when returning to the market. Time kills deals. The longer your home sits, the harder it can be to get your full asking price again.

And yes, you’ll need to disclose the failed contract to new buyers.

Smart Listing Strategy Starts with Your Agent

Smart Listing Strategy Starts with Your Agent

You can’t anticipate every twist in a transaction—but you can stack the odds in your favor by aligning with a real estate professional who understands the risks and has strategies to handle them.

That’s where I come in.

I’m Robbie English, Broker and REALTOR at Uncommon Realty. I’ve spent decades navigating the real estate industry from every angle—working with buyers, sellers, investors, and agents. I’m also a national real estate speaker and instructor, teaching agents across the country how to master their craft and serve clients better.

I’ve made it my mission to master the process, so my clients don’t have to absorb the consequences of others’ inexperience.

When it comes to what happens if buyer’s loan is denied, I’ve seen the scenarios play out in every possible way. And I’ve built systems to avoid the worst outcomes.

What to Do Immediately If a Buyer’s Loan Is Denied

Let’s say your worst fear becomes reality. You get the call. The lender denied your buyer at the last minute. What now?

First, don’t panic. Then move quickly.

-

Notify your listing broker immediately—preferably one like me, who knows how to act fast.

-

Request written documentation from the buyer’s agent or lender that explains the denial.

-

Evaluate your legal position in the contract. Did the denial occur inside or outside the financing contingency?

-

Decide whether to pursue the earnest money or release it, depending on your goals.

-

Relist the property only after reviewing your pricing, staging, and timing to ensure it enters the market strong.

Speed is crucial. The longer your property sits inactive, the more the market begins to question it. But don’t rush. Make your next steps strategic.

Understanding Contingency Clauses

Most sales contracts include a financing contingency. This clause protects the buyer in case their loan is denied. But it also creates a window of risk for the seller. Many agents gloss over this detail. I don’t.

I analyze every clause in the contract with my clients. If the financing contingency ends in 14 days, I know what to expect on day 15. If the buyer tries to terminate after that, we assess our legal rights carefully and act in your best interest.

Too often, sellers operate with vague information or hopeful assumptions. I don’t allow that. You deserve clarity.

Relisting After a Buyer Loan Denial

If you do end up relisting, it’s not the end of the world—but it must be done smartly. Presentation, timing, and positioning are everything.

We’ll review every piece of your listing:

-

Was the buyer’s denial based on price? We’ll reevaluate whether adjustments are needed.

-

Did your marketing speak clearly to your home’s strengths? If not, we rework it.

-

Does your pricing align with current showing activity? Let’s make it irresistible to the next buyer.

My goal? To ensure your property returns to the market with power—not desperation.

How I Help Sellers Protect Themselves

You can choose any agent. But not all agents can offer what I do.

I’ve built my practice around education, precision, and preparation. I help my clients think two steps ahead—not just react when something goes wrong.

When we list your home, I don’t just market it. I scrutinize every offer that comes in, reading between the lines. I call lenders. I ask questions that many agents don’t even think to ask. I look for signals of financial instability before we accept anything.

That’s what decades of experience provide: the ability to spot trouble early and course-correct fast.

In Real Estate, Details Matter

There’s no room for autopilot in a real estate transaction. Not when hundreds of thousands—or even millions—of dollars are at stake.

Whether it’s identifying red flags in a buyer’s financing or negotiating backup offers that give you leverage, I approach every sale as if it were my own.

Because I know what happens if buyer’s loan is denied. And I refuse to let that catch my clients by surprise.

Final Thoughts

You deserve a seamless closing. You deserve a buyer who is ready, qualified, and guided by professionals who get the job done. Unfortunately, the real estate world doesn’t always hand you that—sometimes you have to fight for it.

That’s where the right representation makes all the difference.

Don’t let buyer financing falling through disrupt your future plans. And don’t go into any transaction without knowing what happens if buyer’s loan is denied.

Let’s work together to make sure your sale doesn’t just close—it closes smart.

Leave a Reply